Editor's Note: The following article hasbeen contributed by Scott Palmer, president & CEO ofInjury Sciences LLC.

|Predictive analytics is a valuable tool and is being applied toa growing number of areas in auto insurance operations. Inrecent months, I have fielded questions about the benefit ofapplying predictive analytics to a combination of auto physicaldamage data and medical data to identify questionableinjuries.

|To be sure, predictive analytics has shown benefits in claimsoperations by improving fraud referrals, identifying subrogationopportunities and “right tracking” claims assignments. Consequently, on the surface, the approach sounds appealing. However, a closer look into what predictive analytics can offer andthe constitution of the data employed reveals a problematiclandscape.

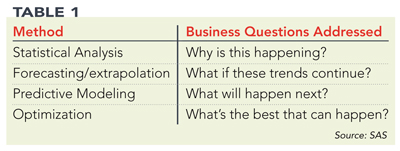

|In the book “Competing on Analytics,” authored by Tom Davenportand Jeanne Harris, analytics is described as “the extensive use ofdata, statistical and quantitative analysis, explanatory andpredictive models and fact-based management to drive decisions andactions.”

|Further, in the table below, Davenport and Harris outline asuccinct progression of business analytics and intelligence.Note the table presented in “Competing on Analytics” wasadapted from a graphic produced by SAS and used withpermission. Each method presented requires increasingsophistication—that is, optimization is a more sophisticated levelthan predictive modeling.

|

In the deployment of analytics, most will concur that theusefulness of results will depend greatly on the quality of thedata, the appropriateness of the data analysis, and the quality ofassumptions employed. It is also important to note that whenmodels are properly deployed, they do notprovide answers. Rather, theyyield information about a tighter distributionon possible outcomes.

|'Smoke Alarms' for Claims Organizations

|Some have suggested the opportunity to use predictive analyticsto identify problematic or questionable injury claims is analogousto providing a claims organization a “smoke alarm.” Theanalytics alert one to a problem early before it becomes a biggerproblem. This analogy, while inaccurate, is actuallyinstructive regarding the proper use of predictive analytics.

|A smoke alarm detects smoke, which is an outcome that iscaused by an actual fire. Hopefully italerts one of an actual fire before it becomes a biggerfire. Alternatively, effective predictive analyticsapplications are more consistent with alerting one to conditionsthat are favorable for a fire taking place. One would want toinvestigate the actual existence of the fire before takingaction—calling 911, activating a fire suppression system, and soon—because there can be considerable costs to such actions ordecisions when there are false alarms. Alternatively, thereare also instances when a fire does not matter because it may be abetter outcome to just let it take its course if it in factdevelops.

|So, while there still may be value in knowing favorableconditions for a fire exist early, an investigative step or processis usually recommended to confirm the actual existence or potentialimpact of the problem before decisions are made to act on theinformation. This is why in fraud analytics applications,fraud investigations are usually conducted after potentiallyfraudulent claims are flagged and before final decisions aboutfraud are made. In subrogation applications, subrogationopportunities are normally further evaluated before being actedupon.

|Investigation Beyond Analytics

|Let's examine why further investigative steps might be requiredwhen basing analytics, in part, on medical data. Medical datausually available to the auto insurance industry is accumulatedfrom injury claims presented by claimants, their attorneys or theirmedical care providers. This information is often audited forreasonableness and appropriateness, in both first and third-partyinjury claims. The entire process of collecting the dataassumes that the basis for the claim, specifically theauto accident, actually caused the claimed injury and theneed for treatment. Next, we will explore how this assumptioncreates the opportunity for the data to include outcomes not causedby the accident (no causality) and outcomes that includeover-treatment of an injury potentially caused by the accident (oneform of an abuse in the system).

|The assumption that causation exists is actually perpetuated bymedical providers. Physicians, for example, are classicallytrained to take a history from the patient, conduct a physicalexamination, and then incorporate the findings of the previous twosteps into his/her diagnosis and treatmentrecommendations. Therefore, if someone claims that a conditionis directly related to an auto accident, then the physician factorsthis information into his or her treatment plan and cites the autoaccident as the cause.

|This problem is further compounded when the treatment plan istailored to the severity of the injury as perceived by the medicalprovider, not by an analysis of the severity of the collision andthe imparted stresses and strains. Subsequently, treatmentguidelines are often used, regardless of the severity of theimpact—in terms of collision energy—to identify when treatment isreasonable and appropriate. However, this practice still helpsidentify other forms of abuse in the system.

|Flaws In Medical Data

|These real-world practices begin to illuminate the flaws in themedical data maintained by auto insurance companies and theirservice providers: Medical treatments are often not prescribedor subsequently evaluated in light of the physical events requiredto produce the need for them. This flaw is inherent in thedata maintained by utilization review or medical auditproviders. From a scientific perspective, injuries areactually caused by a very specific physical stress orstrain, or specific combinations of stresses and strains unique tothe injury. These requisite stresses and strains can be foundto exist (or not exist) based on an analysis of the physics(vehicle accelerations or decelerations) of the accident. Aninvestigation would also take into account the position of theoccupant in the vehicle, the use of restraint systems, and variousother factors. Additionally, when requisite stresses andstrains exist, they still must exceed an individual's tolerance tosame, before the injury can be caused.

|Reliable Models To Assess Injury Claims

|Without such a scientific analysis, how can a professionaldetermine which medical data within a data set isquestionable? Wouldn't this knowledge be required to build asound model to identify questionable claims so that auto physicaldamage relationships can be developed for both groups?

|From a holistic view, it would also seem there would be muchlearned about questionable injury claims by understanding data ininstances when injuries are not claimed as a result of anauto collision. The good news is that accidents that do notcause injuries occur very frequently. This outcome iscorroborated by human subject testing in low-speed crashtests. More than 75 percent of the approximately 4,000scientific human subject test exposures known to the authorproduced no injury. The bad news is that little claim data istypically collected by an insurer on an uninjured passenger when aninjury claim is not made and no injury feature iscreated.

|Sometimes no data is available because no claim is made as aresult of an accident. Wouldn't some information about thecondition and physical attributes of the individual not makingan injury claim, his or her seating position in the vehicle,use of available restraint systems, and so on be relevant to areliable model that predicts questionable injury claims? Othertimes, injuries occur but data collected is incomplete becausethere is a determination that there is either no coverage orliability. Again, wouldn't more complete information underthese circumstances be important to a reliable model?

|Combining Auto Physical Damage and MedicalData

|Structurally, one can begin to see how trying to applypredictive analytics to a combination of auto physical damage dataand medical data to identify questionable injuries can beproblematic. To illustrate, let's examine ahypothetical temporomandibular disorder (TMJ) injury claim from alow-energy frontal collision from a statistical and scientificperspective. Statistically, data will exist that involveaccidents with varying degrees of physical damage to the claimant'sautomobile accompanied by a TMJ injury claim.

|Most likely, these injuries will be observed at a low to verylow incident rate. Data will also likely show reasonable andcustomary costs for treatment of the TMJ injury and likely reflect deviations fromthese standards. So, does the statistical model suggest theinjury should be questioned? If so why, then why? Was thisbecause a treatment period was too long or not properly coded? Or,perhaps the medical provider was not a physician? What about thelocation of the clinic? What gives the claims adjuster thebasis to make a decision or take an action and defend it?

|Scientifically, the answer is straightforward. Totraumatically injure TMJ, there must be contact between themandible and an object with sufficient force to create the stressesand strains to cause injury. Simply, if there is no mandiblecontact with an object, then there is no opportunity for a TMJinjury (none of the previously referenced human subject testexposures experienced a mandible strike or a TMJ injury). Canan occupant in a vehicle involved in a frontal collision strike hisor her mandible on an object? It is certainlypossible. The answer becomes clearer once we know where theoccupant was seated in the vehicle and whether he or she wasrestrained. Incidentally, both of these critical facts aretypically not found in the medical data.

|'Old School' Attributes

|The scientific analysis as described above can be applied to avariety of injuries, including neck, back, shoulder and knee, toactually determine when questionable injuries were (or were not)caused from a collision. To use a popular example illustratedin the book Moneyball by Michael Lewis, there was an importantdifference in the predictive outcome in baseball games between the“old school” use of batting average to evaluate players and neweranalytics using on-base percentage. Whileadmittedly not a perfect analogy, using medical data in theproposed approach in lieu of scientific analysis certainly has many“old school” attributes.

|So what can be done? First, understanding thelimitations of the data and the resulting implications arecritical. Use of statistical methods for dealing with unknownsand data limitations is common in predictiveanalytics. However, when these methods are used in claimsapplications, they should be followed by investigative processesthat resolve the related unknowns and validate the assumptionsemployed. In the instance of questionable injury claims, anassessment of causality and, when appropriate, an analysis ofpotential abuses in the system can help the decision maker moreconsistently reach accurate outcomes.

|Secondly, there is an opportunity to improve the data collectedwhen there is no injury claim made in an accident. Based on the TMJinjury example previously provided, collection of scientificallyrelevant facts during a claim investigation can, over the longterm, help offset many of the significant limitations found in themedical data. Third, consider using analytics that, while notconsidered as only predictive analytics, actually define anddescribe the event in an accurate and defensible way. Forexample, referring back to the book “Competing on Analytics,” oneform of analytics described was employed by VisViva Golf Inc. Thecompany uses nanotechnology embedded in golf clubs that isconnected to Bluetooth radio technology to calculate and measuretechnical aspects of a golfer's swing—the swing speed,acceleration, deceleration, and so on—as well as use the data withpredictive analytics to provide guidance to improve the golfer'sswing.

|Today, automated analytics are available for claimsorganizations which scientifically predict or actually determineacceleration and deceleration of vehicles in accidents and theresulting implications to injury potential—or, in other words,scientifically identify questionable injuries. More specifically,the scientific analytics described in the previous TMJ example canbe systematically applied to claims data such as repair estimateinformation and injury claim information.

|In conclusion, using medical data in predictive analyticsapplications to identify questionable claims could be, well,questionable. While all the numbers and formulas associatedwith today's analytics suggest objectivity, experienced managersunderstand that the “garbage in, garbage out” phenomenon has neverbeen truer. Realizing the power of analytics requires beingrealistic about what models can and cannot do, improving thequality of the data feeding models, and creating theappropriate managerial processes around them.

|In the context of injury claims, statistical models basedon medical data should be accompanied by an investigative processthat will provide an adjuster with actionable information and thebasis for defensible decisions. Otherwise a claims organization mayfind itself in a position of systematically creating more firesthan they are trying to avoid. The use of predictive analyticsin this approach begs the following: Why not use defensibleanalytics in the identification of questionable claims? Would thisnot eliminate an unnecessary step?

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- All PropertyCasualty360.com news coverage, best practices, and in-depth analysis.

- Educational webcasts, resources from industry leaders, and informative newsletters.

- Other award-winning websites including BenefitsPRO.com and ThinkAdvisor.com.

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.